Beat financial barriers

Become your own financial hero

Become the master of your financial destiny and unleash the superhero within you. Take charge of your financial well-being, make smarter choices, and soar to new heights of financial freedom.

As Seen On

Meet Peter

Peter, a best-selling author and multi award-winning financial content creator, TV personality, and speaker, empowers people to achieve financial security. His journey from foster care, to a Fortune 100 executive includes overcoming homelessness in his teens and becoming a qualified Financial Adviser and Mortgage Adviser. Peter has held major roles at Natwest/RBS, MetLife, and Investec, sharing his expertise on shows like Secret Spenders, Lorraine, Steph's Packed Lunch, Katie Piper's Breakfast Show, Jeremy Vine, Sky News and Channel 5 News.

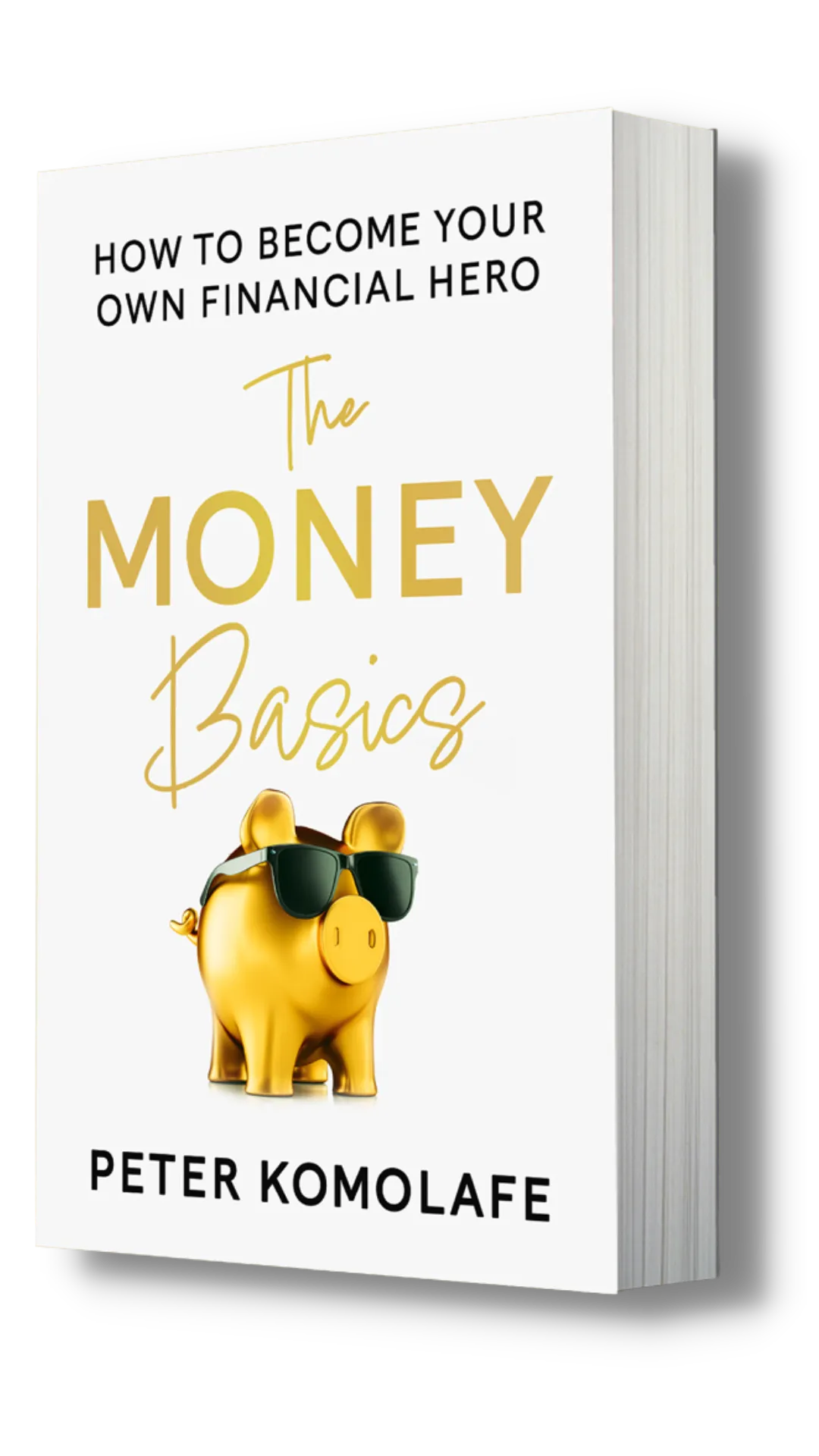

The essential guide to the BASICs of personal finance

Unlock the secret to financial independence and become your own financial hero with the Basic Formula, explained and unpacked in The Money Basics. This is the ultimate guide to mastering your finances and achieving your financial goals.

#1 Best-Seller selected as one of The Sun’s ‘Top Books to Turn the Page on Money Woes’

Individuals

Subscribe to Our Newsletter

Receive a weekly dose of news and financial updates delivered directly to your email inbox.

We never spam, we respect your privacy.